top of page

eduo

visual

Biostatistics & Epidemiology

Health Insurance Models

Core Principle of Health Insurance Models

🧷

Health insurance distributes financial risk of healthcare costs across a population, transforming unpredictable individual expenses into predictable premiums.

🧷

The fundamental tension in all models is balancing three competing goals: universal access, cost control, and quality of care — improving two typically compromises the third.

🧷

Different countries and systems emphasize different priorities, leading to distinct models with characteristic advantages and disadvantages.

🧷

Board pearl: Questions often test recognition of which model a clinical scenario describes based on payment structure, provider relationships, and patient access patterns.

Fee-for-Service (FFS) Traditional Model

📍

Providers bill separately for each service rendered — office visits, procedures, tests — with no bundling or coordination incentive.

📍

Incentivizes volume over value: more procedures → more revenue, potentially leading to overutilization and fragmented care.

📍

Patients typically have freedom to see any provider but may face high out-of-pocket costs through deductibles and coinsurance.

📍

Traditional Medicare and most private insurance operated this way historically, though pure FFS is increasingly rare.

📍

Board clue: If a vignette describes a physician ordering multiple tests "to be thorough" with each billed separately, think FFS incentive structure.

Health Maintenance Organizations (HMOs)

🔹

Closed network model where patients must receive care from contracted providers, with primary care physician (PCP) as gatekeeper.

🔹

Capitation payment: providers receive fixed payment per patient per month regardless of services provided, incentivizing prevention and efficiency.

🔹

Referral required from PCP to see specialists; no coverage for out-of-network care except emergencies.

🔹

Lower premiums and predictable costs for patients but restricted provider choice.

🔹

Board pearl: Patient needs referral to see dermatologist and cannot self-refer → HMO model.

Preferred Provider Organizations (PPOs)

⭐

Hybrid model offering in-network and out-of-network coverage with different cost-sharing levels.

⭐

No PCP gatekeeper requirement — patients can self-refer to specialists without prior authorization.

⭐

Higher premiums than HMOs but greater flexibility in provider choice.

⭐

In-network care has lower copays/coinsurance; out-of-network care is covered but with higher patient cost-sharing.

⭐

Board distinction: PPO = flexibility without referrals; HMO = lower cost with gatekeeping.

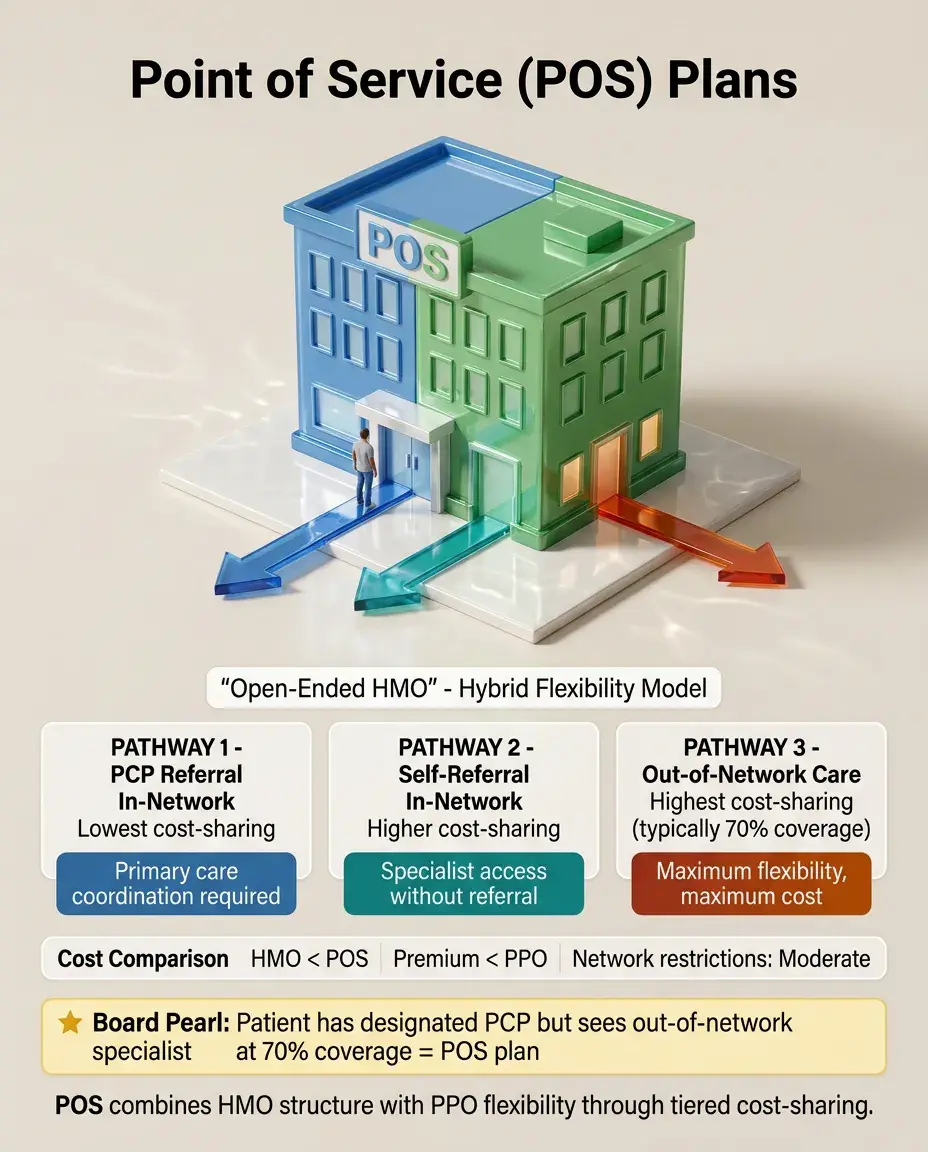

Point of Service (POS) Plans

✅

Combines HMO structure with PPO flexibility — requires PCP designation but allows out-of-network care at higher cost.

✅

In-network referrals from PCP have lowest cost-sharing; self-referral to in-network specialists costs more; out-of-network care most expensive.

✅

Often called "open-ended HMO" because it relaxes strict network restrictions.

✅

Premium typically between HMO and PPO levels.

✅

Board clue: Patient has designated PCP but can see out-of-network specialist at 70% coverage → POS plan.

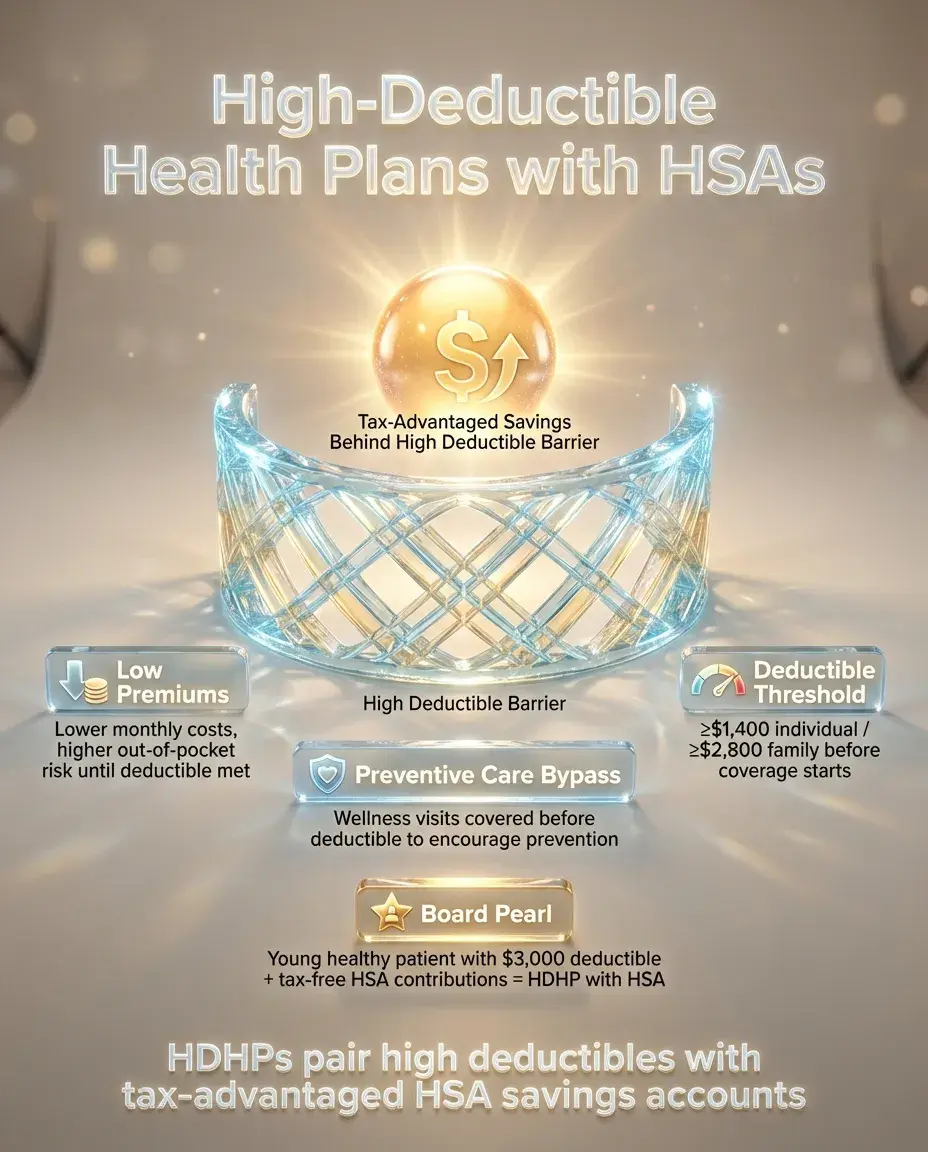

High-Deductible Health Plans (HDHPs) with HSAs

🧠

Insurance with high annual deductible (≥$1,400 individual, ≥$2,800 family in 2023) that must be met before coverage begins.

🧠

Paired with Health Savings Accounts (HSAs) — tax-advantaged accounts for medical expenses that roll over annually.

🧠

Lower premiums but higher financial risk for patients; incentivizes cost-conscious healthcare decisions.

🧠

Preventive care often covered before deductible to encourage wellness visits.

🧠

Board pearl: Young healthy patient choosing plan with $3,000 deductible and contributing to tax-free savings account → HDHP with HSA.

Medicare Structure and Parts

⚡

Part A: Hospital insurance — covers inpatient care, skilled nursing facilities, hospice. Funded by payroll taxes, no premium for most beneficiaries.

⚡

Part B: Medical insurance — covers outpatient services, physician visits, preventive care. Optional with monthly premium.

⚡

Part C: Medicare Advantage — private insurance alternative combining Parts A, B, and usually D.

⚡

Part D: Prescription drug coverage — offered through private insurers with formulary tiers.

⚡

Board distinction: Original Medicare (A+B) = fee-for-service; Medicare Advantage (C) = managed care with networks.

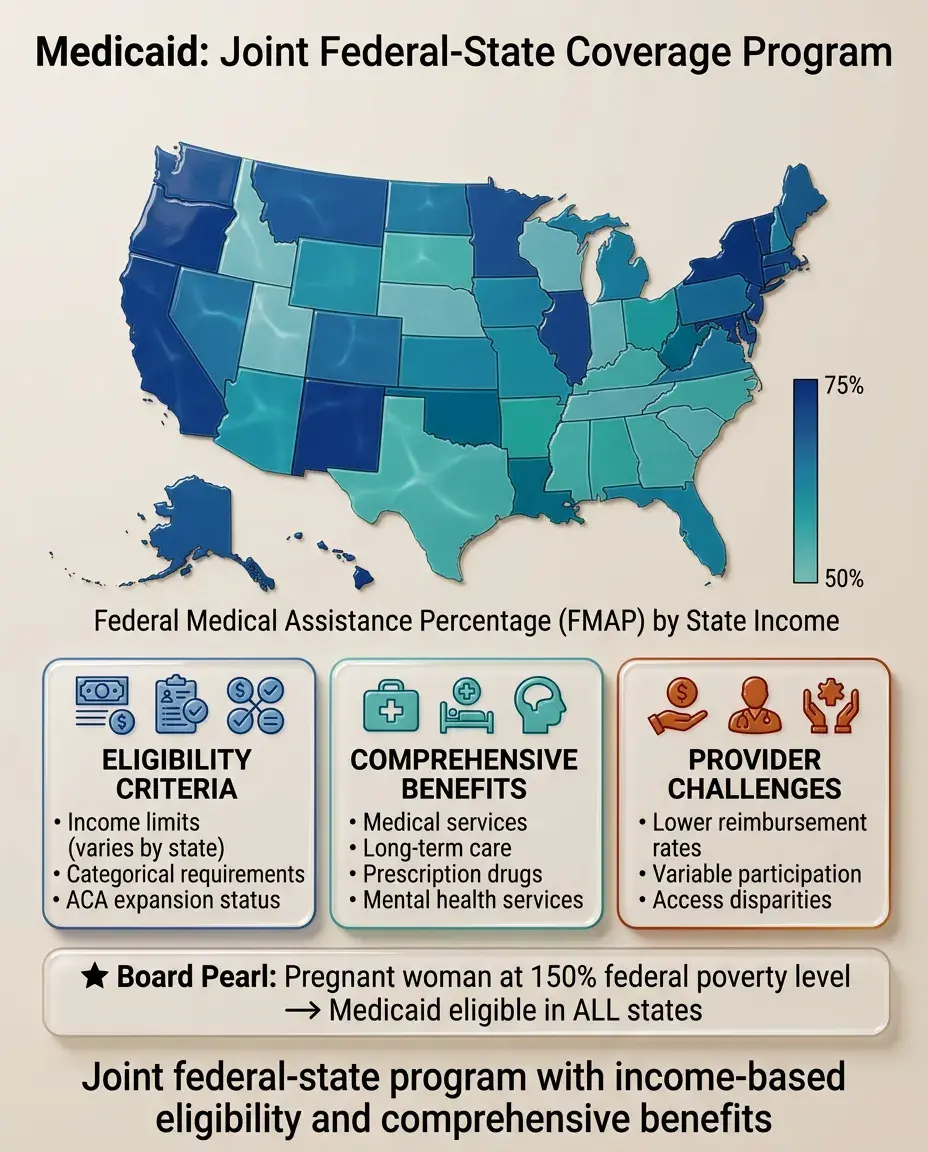

Medicaid Fundamentals

📌

Joint federal-state program providing coverage for low-income individuals and families.

📌

Eligibility varies by state but includes income limits, categorical requirements (pregnant, disabled, children), and ACA expansion status.

📌

States administer programs with federal matching funds (FMAP) ranging from 50-75% based on state per capita income.

📌

Benefits more comprehensive than Medicare, including long-term care, but provider participation varies due to lower reimbursement rates.

📌

Board pearl: Pregnant woman at 150% federal poverty level seeking prenatal care → likely Medicaid eligible in all states.

Single-Payer and National Health Insurance Models

📣

Government acts as sole insurance provider, funded through taxation, with private delivery of care (Canada model).

📣

Eliminates insurance administrative complexity and profit margins; negotiates prices directly with providers.

📣

Universal coverage with no patient bankruptcies but potential for longer wait times for elective procedures.

📣

Not synonymous with socialized medicine — providers remain private unlike UK's National Health Service where government employs physicians.

📣

Board clue: System with universal coverage, no insurance companies, but private physician practices → single-payer model.

Beveridge Model (National Health Service)

🔸

Government owns hospitals and employs healthcare workers directly — true socialized medicine (UK, Spain, Scandinavia).

🔸

Funded through general taxation with care free at point of service.

🔸

Strong cost control through global budgets and salary-based physician compensation.

🔸

Excellent primary care access but potentially long waits for specialist referrals and elective surgeries.

🔸

Board distinction: Government-employed physicians in government-owned hospitals → Beveridge model, not just single-payer.

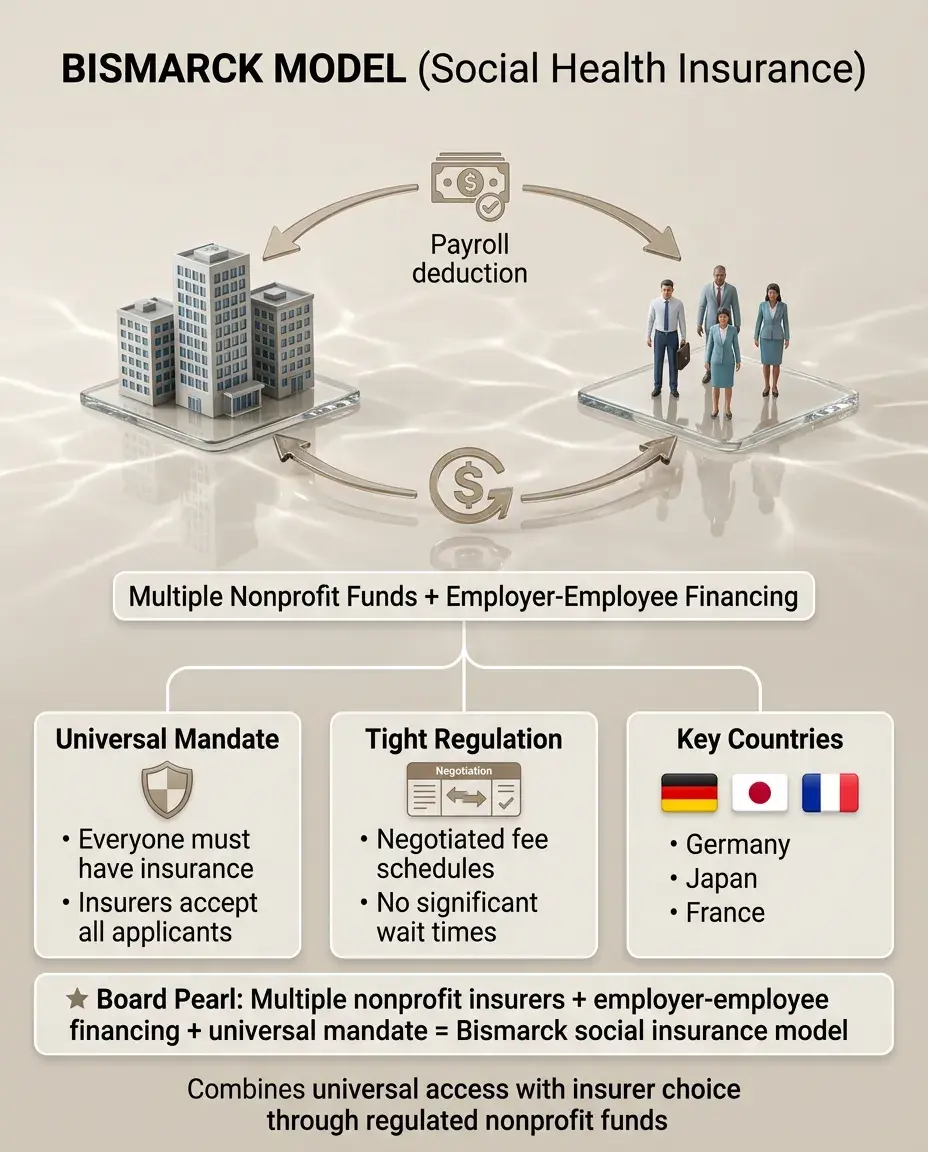

Bismarck Model (Social Health Insurance)

🧷

Multiple nonprofit insurance funds (sickness funds) financed jointly by employers and employees through payroll deductions.

🧷

Universal coverage through mandate — everyone must have insurance and insurers must accept all applicants.

🧷

Tight regulation of insurance funds and negotiated fee schedules with providers (Germany, Japan, France).

🧷

Combines universal access with choice among insurers and no significant wait times.

🧷

Board pearl: Multiple nonprofit insurers with employer-employee financing and universal mandate → Bismarck social insurance model.

Out-of-Pocket Model

📍

No organized insurance system — patients pay providers directly at time of service.

📍

Common in developing countries and rural areas of middle-income nations.

📍

Creates severe access barriers for poor populations; wealthy receive good care while others go without or face financial ruin.

📍

Often leads to two-tier system with public hospitals providing basic care and private facilities serving those who can pay.

📍

Board clue: Patient selling livestock to pay for surgery in country without insurance system → out-of-pocket model.

Accountable Care Organizations (ACOs)

🔹

Networks of providers jointly responsible for quality and total cost of care for defined patient population.

🔹

Shared savings model: ACO keeps portion of Medicare savings if quality benchmarks met while staying under spending target.

🔹

Incentivizes care coordination, prevention, and appropriate utilization rather than volume.

🔹

Providers remain fee-for-service but with bonuses for efficiency and quality.

🔹

Board pearl: Group of hospitals and physicians sharing savings from reducing readmissions → ACO payment model.

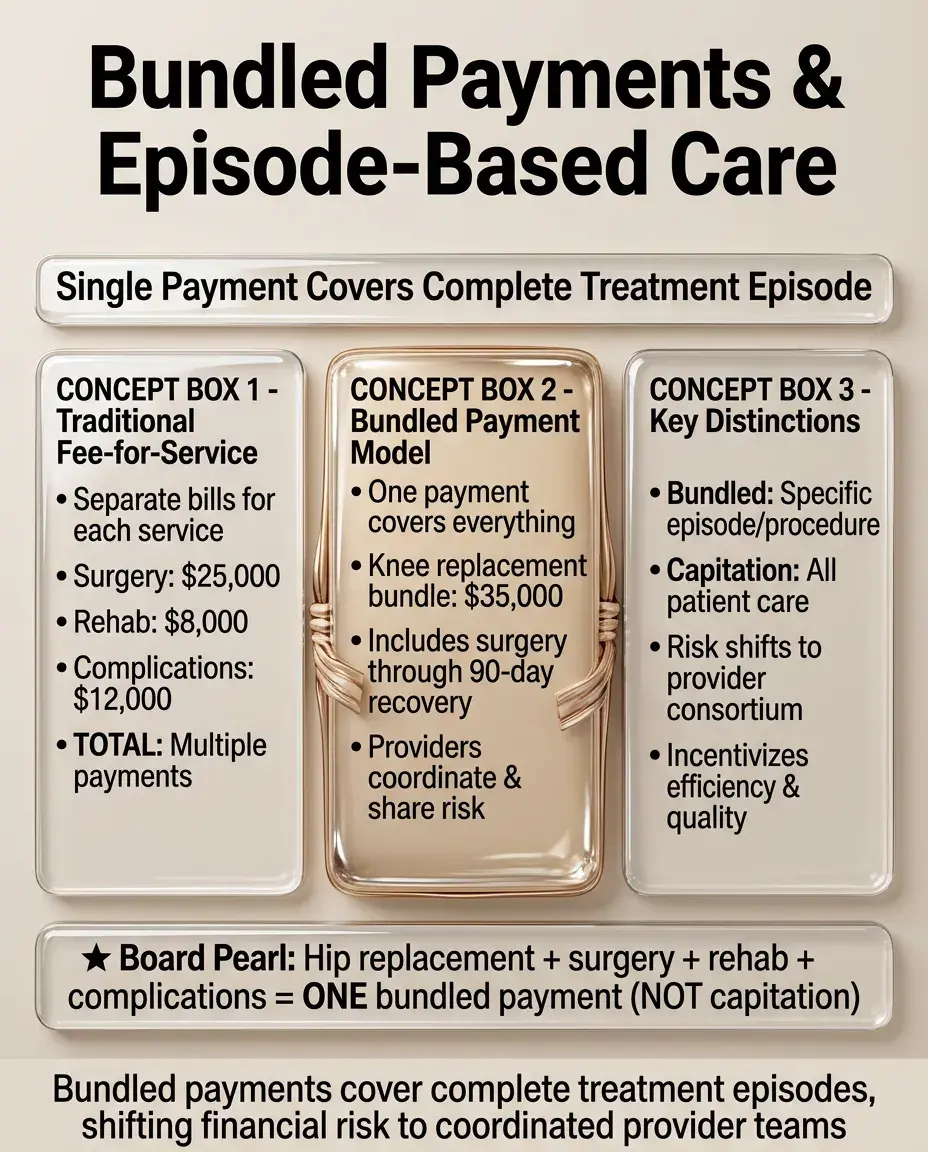

Bundled Payments and Episode-Based Care

⭐

Single payment covers all services for specific treatment episode (e.g., knee replacement from surgery through 90-day recovery).

⭐

Providers must coordinate care and manage costs within bundle — incentivizes efficiency and reduces complications.

⭐

Risk shifted from payer to provider consortium who must allocate payment among participants.

⭐

Different from capitation which covers all care; bundles target specific conditions or procedures.

⭐

Board distinction: One payment for hip replacement including surgery, rehab, and complications → bundled payment, not capitation.

Pay-for-Performance (P4P) and Value-Based Purchasing

✅

Providers receive bonuses or penalties based on quality metrics — clinical outcomes, patient satisfaction, process measures.

✅

Aims to improve quality while controlling costs by rewarding value over volume.

✅

Metrics must be risk-adjusted to avoid cherry-picking healthy patients or avoiding complex cases.

✅

Can create documentation burden and potentially encourage gaming of metrics.

✅

Board clue: Hospital receives 2% Medicare bonus for reducing surgical site infections → pay-for-performance incentive.

Insurance Market Concepts: Risk Pools and Selection

🧠

Risk pooling spreads costs across healthy and sick enrollees — larger, more diverse pools create more stable premiums.

🧠

Adverse selection occurs when sick individuals disproportionately enroll while healthy avoid coverage, creating "death spiral" of rising premiums.

🧠

Risk adjustment transfers funds from insurers with healthier enrollees to those with sicker populations.

🧠

Community rating requires same premium regardless of health status; experience rating allows variation based on risk.

🧠

Board pearl: Young healthy people avoiding insurance until sick → adverse selection threatening pool stability.

Prior Authorization and Utilization Management

⚡

Insurance company review of medical necessity before approving coverage for services, medications, or procedures.

⚡

Intended to reduce inappropriate utilization and control costs but can delay care and increase administrative burden.

⚡

Step therapy ("fail first") requires trying less expensive options before approving costlier treatments.

⚡

Appeals process allows providers and patients to challenge denials with additional documentation.

⚡

Board clue: Physician must document failed conservative treatment before MRI approved → prior authorization requirement.

COBRA and Insurance Portability

📌

COBRA (Consolidated Omnibus Budget Reconciliation Act) allows temporary continuation of employer coverage after job loss at full premium cost.

📌

HIPAA (Health Insurance Portability and Accountability Act) prohibits pre-existing condition exclusions for those with continuous coverage.

📌

ACA marketplace provides alternative to COBRA with potential subsidies based on income.

📌

Gap in coverage can lead to pre-existing condition waiting periods in non-ACA compliant plans.

📌

Board pearl: Recently unemployed patient asking about keeping insurance → COBRA continuation rights for 18-36 months.

Board Question Stem Patterns

📣

Patient needs referral from primary doctor to see specialist → HMO model

📣

Physician employed by government in public hospital → Beveridge/NHS model

📣

Multiple nonprofit insurers funded by payroll taxes → Bismarck social insurance

📣

Patient choosing between in-network and out-of-network cardiologist → PPO plan

📣

Hospital receiving one payment for entire hip replacement episode → bundled payment

📣

Young patient with $5,000 deductible contributing to tax-free account → HDHP with HSA

📣

Provider group sharing Medicare savings from care coordination → ACO model

One-Line Recap

🔸

Health insurance models balance access, cost, and quality through different mechanisms — from single-payer systems eliminating insurance overhead to managed care restricting networks, from fee-for-service incentivizing volume to capitation and bundling promoting efficiency, with the U.S. uniquely combining multiple models including employer-based insurance, means-tested programs (Medicare/Medicaid), and market-based reforms emphasizing value over volume.

bottom of page